On 15 August, we celebrated an important anniversary, even if it did not make the headlines, a half-century anniversary, the figure is symbolic, that of the suspension of the convertibility of dollars into gold, proclaimed by Richard Nixon on 15 August 1971 during a televised speech. A suspension announced at the time as temporary, which is not without irony, but we were then moving into uncharted territory.

This was a fundamental shift because money had always been linked to gold or silver. It even identified with it for centuries through the coins that circulated, or documents that attested that they represented such weight in gold, which allowed the development of banking. With the Bretton Woods Agreements signed in 1944, we were no longer in a strict gold standard as in the nineteenth century but in an unbalanced system where gold and the dollar had the same status of reserve currency, in a ratio of 35 dollars per ounce (31.1 grammes) the other currencies being in the background. The writing was on the wall and the temptation was great for the United States to make the dollar the only reserve currency in the world and to free itself from the constraint of gold, which it then went on to do half a century ago.

However, we must not idealise the past, the period before 1971 did not constitute a monetary “golden age”, manipulations have always existed: gold coins were chipped, their gold content fell without their face value changing, the strict gold standard did not prevent banking crises (end of the 19th century), the reintroduction of the gold standard without taking into account the inflation due to the First World War caused serious imbalances during the interwar period. But, despite everything, the physical limitation of the quantity of gold available was a constraint, whereas now the dollar and the major currencies can be printed without limit. We speak of “fiat money”, the term fiat being a Latin word meaning “let it be done”, which is found in the expression “fiat lux” (“let there be light”) used by God in Genesis.

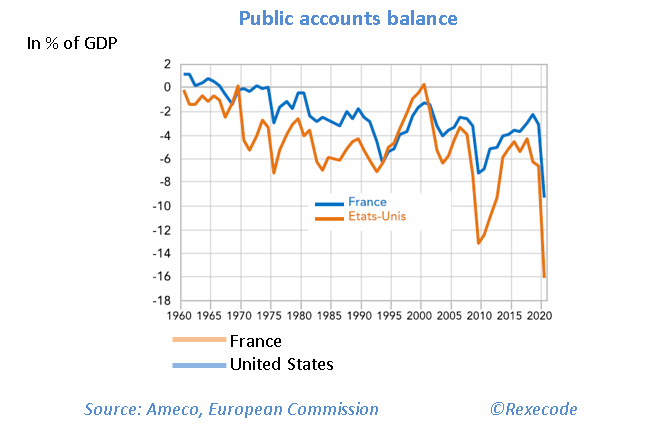

What we have lost with the gold standard is a safeguard, moving towards a regime where money can be created according to need without structural limits. However, this is not without risk. Inflation, although brought under control today, can easily turn destructive. Beyond the dispossession of savers, it can erode purchasing power, create shortages and disrupt the economic calculations of entrepreneurs, to the point of casting doubt on the value of the currency, in the worst scenario. To regain a lasting balance, states must imperatively reduce deficits and establish a timetable for the end of stimulus plans which, although they make it possible to deal with an exceptional situation, have the disadvantage of increasing the debt. Growth can also be found in lowering the level of taxes and levies, and in simplifying standards and bureaucracy.

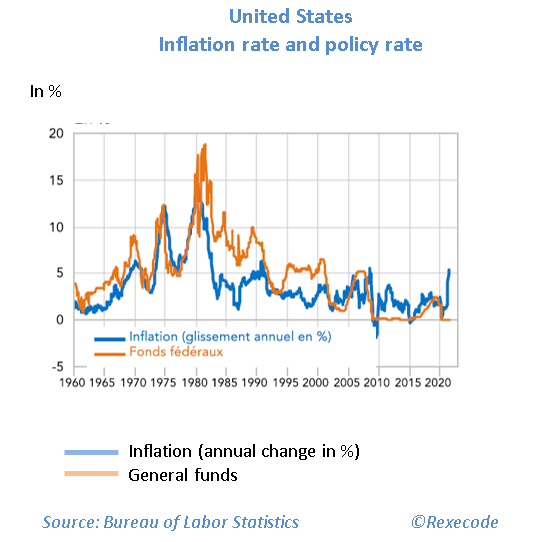

Therefore, a healthy situation comparable to the 1980s and 1990s could be restored. In brief, we should be much more careful with money and impose a discipline comparable to that of the gold standard, even if it means adopting more modern criteria. The experiment of a dollar having no other reference than itself almost came to a rapid end with the price change of the 1970s (13.5% inflation in 1980 in the United States). However, energetic central bank (Fed) boss Paul Volcker increased the policy rate to 20% in 1981, a staggering figure today, and he brought inflation under control within a few years.

The 1980s and 1990s combined low price increases, economic growth and the relative stability of the price of gold, between 300 and 400 dollars an ounce, as if we had returned to a de facto gold standard … But how can we explain this? The inflation of the 1970s having served as a lesson, states contained their deficits, reformed (except France), real interest rates were high (which corresponds to a normal situation), and the growth of the economy was not based on debt but came from the deregulation of important sectors such as telecoms (which will give birth to the internet and the mobile phone), the airline sector (explosion of mass tourism); it is the supply policy started by Ronald Reagan and Margaret Thatcher. Organic growth and healthy currency were the reasons why we had returned to a quasi “gold standard”.

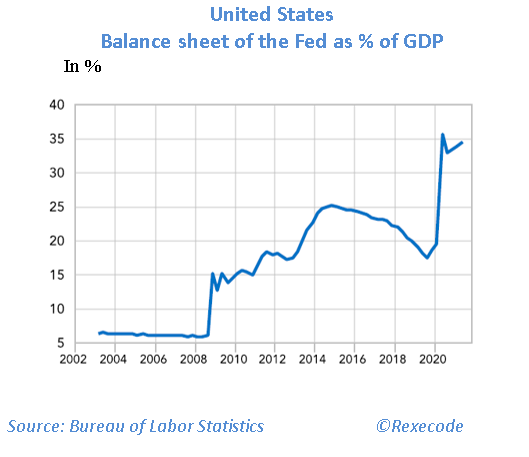

A total turnaround occurred at the beginning of the new millennium with the crash of technology stocks in 2000 and the attacks of 11 September 2001: in an attempt to avoid a depression, the Fed sharply cut its policy rate , money became “free”. A mortgage bubble followed, facilitated by a deleterious financial innovation, the subprimes, and we know the rest of the story with the crash of 2008. The debt crisis of the eurozone in 2010-2012 brought the European Central Bank (ECB) to follow the Fed’s policy. The price of gold evolved to progress from 2002, then especially 2005 to pass from 400 dollars an ounce to nearly 1,900 dollars in August 2011. The central banks took matters in their own hands, managed to reassure, and gold fell in 2013 and 2014, but resumed its progression from mid-2018. Then the emergence of the Covid-19 pandemic and the lockdowns caused budget deficits to explode and led central banks to spin the printing press to an unprecedented level.

This is where we are now, and the novelty of recent months is the return of inflation: the United States is on an average trend above 5% per year, Germany is at 4%, France should soon pass the 2% mark. The problem is that it is now impossible to do what Paul Volcker did in his time, that is to say to significantly increase the policy rate to defeat inflation, there is indeed such an amount of debt, both public and private, that the entire monetary and financial system would face a terrible crisis.

Sources : Rexecode, Banque Delubac & Cie, Refinitiv, Ameco, Commission européenne, Bureau of Labor Statistics