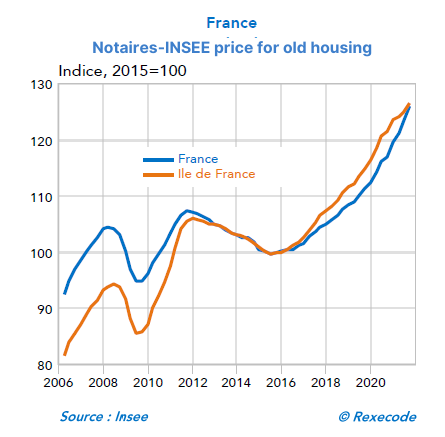

Real estate in France has been experiencing a rise in prices since the early 2000s. The Covid pandemic, with the fall in GDP that followed the confinements, has not reversed this trend. In Europe, despite the specificities of each market, prices are also rising to a greater or lesser extent, even in Germany, which had long been spared.

The fundamental cause is the expansionary policy of the European Central Bank (ECB): the quantity of money is increasing more rapidly than the volume of goods and services available, consequently prices rise. Not mechanically of course, because at the same time the speed of the circulation of money is falling (during the Covid, savings have increased, money is “frozen”), which mitigates the progression of prices. But in recent months, we have experienced unprecedented levels of money creation..

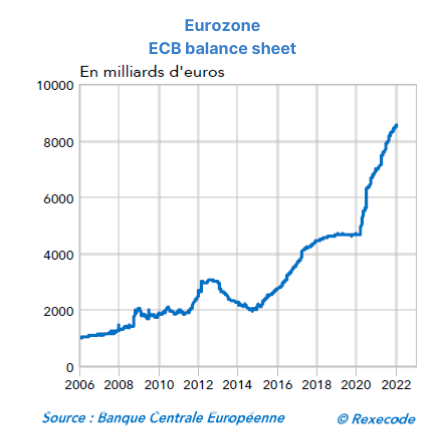

The balance sheet of the ECB has increased by more than 3,000 billion euros since the start of the Covid crisis, from 5,000 to more than 8,000 billion euros. It is literally money created ‘out of nothing’, by a paper exercise, in order to subscribe to the loans issued by the States facing the gigantic deficits caused by the pandemic. There had been so-called “money printing” before, during the subprime crisis of 2008, then during the Greek debt crisis in 2011, but the current period far exceeds them both. The ECB’s balance sheet total is equivalent to 81% of Eurozone GDP, compared to 37% for the Fed, 41% for the Bank of England. Only the Bank of Japan has more (134%), but the debt is entirely held internally, which changes the situation. The vertiginous rise we are witnessing is not about to stop as the budget deficits in France and in the countries of southern Europe remain high and are slowly being reduced.

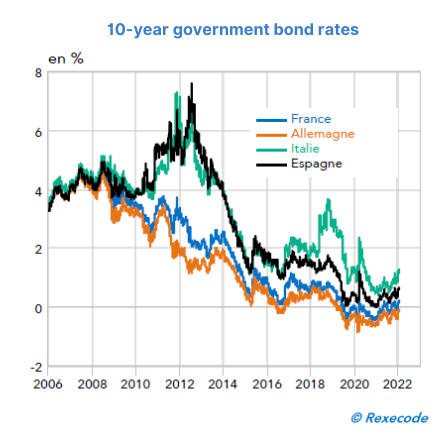

It is very likely that monetary policy in the eurozone will remain expansionary in the years to come, for several reasons:

– the sustainability of public debts must be ensured, a rise in rates would strangle several countries and push them into default;

– it is necessary to allow the financing of the energy transition, which is very costly. Moreover several countries, including France, are beginning to issue “green bonds” for this purpose;

– the current rise in inflation is considered by the ECB to be transitory, and therefore does not call for a change in direction.

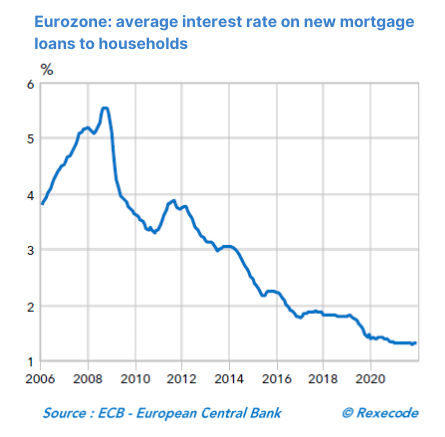

These low rates which, with the return of inflation, bring negative real interest rates, will cause an increase in the prices of real estate, stocks, cryptocurrencies and real assets in general (gold, works of art, vintage cars). Indeed, these assets cannot be “printed”, Picasso paintings or Ferrari Daytonas are no longer produced, and gold or real estate increase very little from year to year, so they constitute safe havens to preserve purchasing power over time. Stocks and Bitcoin are volatile and put many investors off, the art market is complex, so real estate is the investment choice for most savers and for many investors.

As a result, housing prices will continue on this rising trend and, except for those who already have significant assets, this is not good news, for several reasons:

- it makes access to housing difficult for young people and the middle classes;

- wealth inequalities will increase, generating a feeling of injustice and protests;

- such a rise runs the risk of a financial crisis if real estate prices ever drop.

In addition, the energy transition generates heavy constraints: “Technically, the bans on renting ‘energy strainers’ could remove 3 million housing units from the rental stock, including 700,000 in 2025 alone!” according to Jean-Marc Torrollion, President of the FNAIM (French Federation of Real Estate), with many owners recoiling from the cost of the work. And when supply is restricted, prices increase, in this case for rental, but energy saving standards will also make construction more expensive.

Commercial real estate will also be impacted: from 1 January 2022, landlords and occupants of surfaces of more than 1,000 m² will be forced to reduce their energy consumption on the basis of those of 2010 by -40 % by 2030 (i.e. in just 8 years), on the pretext that buildings represent 25% of greenhouse gasBlockchains using smart contracts, such as Avalanche or Ethereum, have several tokens, so is gas. Gas is used

to pay transaction fees or to carry out smart contract operations. Lire la suite emissions in France.

What are the means of action to slow down or stabilise property prices?

- The ECB renouncing its expansionary monetary policy, but this scenario is not very credible, as default on sovereign debt constitutes too serious a risk;

- Use the macroprudential regulation of banks (increase in capital requirements associated with mortgage loans) in order to restrict credit demand. The effect will be limited because the incentive to invest in real estate will remain strong (inflation will not be so transitory, as stated Jerome Powell, Chair of the US Federal Reserve);

- Tax real estate capital gains more heavily, with the underlying idea, still very popular in France, of “making the rich pay”. This measure would nevertheless be costly in terms of votes, and have limited effect, as the remaining capital gains would in any case be a better option than letting your money lie dormant.

As we can see, there is no real solution to the excessive rise in real estate prices due to a durably expansionary monetary policy. We will have to deal with and accept the disadvantages of this situation: difficulty in accessing housing, increase in wealth inequalities, risk of financial crisis in the event of a market downturn. However, a market with rising prices is also an opportunity, of course, even if the level of risk increases. The housing market will become more difficult, but also more exciting!

The balance sheet of the ECB: https://twitter.com/Schuldensuehner/status/1463155482659540996

“Technically, the bans on renting ‘energy strainers’ could remove 3 million housing units from the rental stock, including 700,000 in 2025 alone!”, according to Jean-Marc Torrollion, President of the FNAIM

From 1 January 2022, landlords and occupants of surfaces of more than 1,000 m² will be forced to reduce their energy consumption on the basis of those of 2010 by -40 % by 2030 (i.e. in just 8 years), -50 % by 2040 and -60% by 2019