THE ECB AND THE FRED RAISE THEIR RATES. WHAT WILL BE THE OUTCOMOE OF THIS REACTION ?

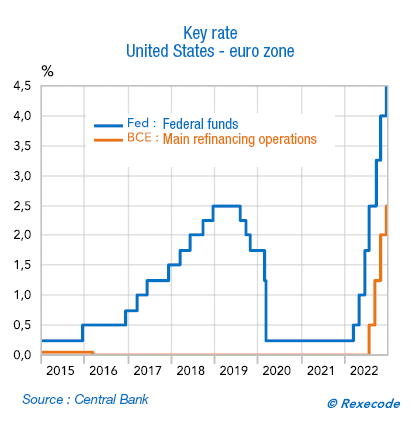

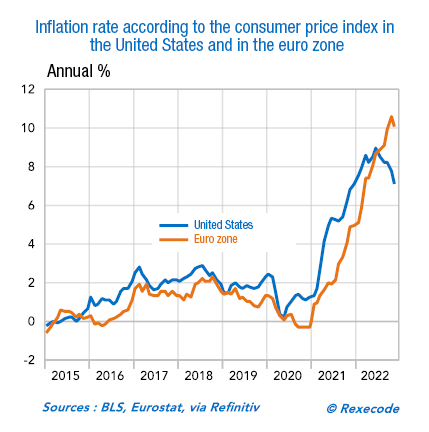

Faced with the return of inflation, central banks reacted by raising their key rates. After holding it at zero for a long time, the US central bank (Fed) raised its key rate to 4.25-4.50% – and further increases are expected – while the European Central Bank (ECB) has begun the same manoeuvre, at 2.00-2.50% today; further rises are expected.

The rise in key rates makes money more expensive, interest rates rise, credit is restricted, global demand decreases and, to adapt, supply falls by lowering its prices. Inflation is then slowed down, at the cost of a more or less significant recession. But it is not always so simple, especially if a price-wage spiral starts (as during the 1970s), with rising wages fuelling price rises without the monetary authorities being able to do much about it.

We already note that inflation in the United States seems to be stabilising at 8%, giving hope for a decline. On the other hand, the euro zone has just crossed the symbolic bar of 10% without any sign of slowing down. How can we explain this discrepancy?

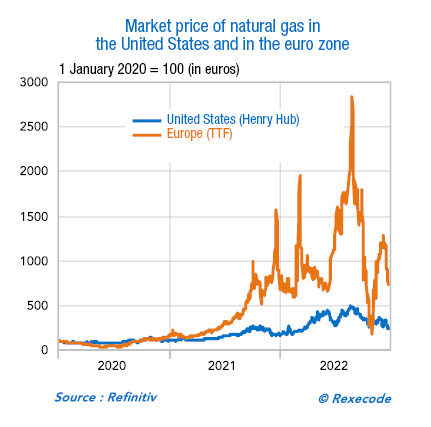

These two major economic areas turn out to be in very different situations in the face of the energy crisis we are going through: the United States is energy independent, thanks to the exploitation of gasBlockchains using smart contracts, such as Avalanche or Ethereum, have several tokens, so is gas. Gas is used

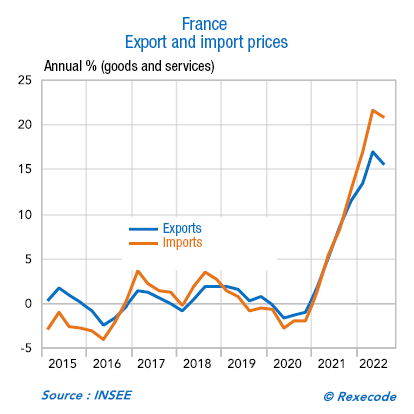

to pay transaction fees or to carry out smart contract operations. Lire la suite and shale oil, unlike Europe, which is highly dependent and therefore correspondingly poorer. Its imports are increasing in value while its exports are slowing down as its competitiveness deteriorates with the rising costs of raw materials and energy. The double penalty for Europe, which sees its trade balance plunge into the red.

While the price of oil is relatively uniform worldwide, because it is easy to transport (supertankers), the price of gas is very heterogenous due to transport costs (by gas pipelines or by liquefaction for LNG). The United States therefore benefits from very low gas prices while, in Europe, the price is very high. As a result, Tesla calls into question the construction of its battery factory in Berlin to repatriate it to the USA. In France Safran suspends the construction of its new factory while Duralex stops its production of glassware for several months, examples abound.

This deterioration in the terms of trade depreciates the euro against the dollar, which makes the raw materials that must be paid for in dollars all the more expensive, this is called “imported inflation”. The ECB’s delay in raising its rates also explains this depreciation.

In the end, the ECB faces a much more complex situation to manage: the rise in interest rates can accentuate a recession without improving anything on the inflation front, which essentially depends on energy prices. It must also act more tactfully, taking into account the debt of the more fragile countries of the South, while the Fed only has to worry about the federal debt. It seems that, in Europe, inflation is here to stay, and even to increase if the euro devalues further.

Sources : Rexecode, Banque Delubac & Cie, Standard and Poors, Euronext Paris, Eurostat, S&P Global, Iboxx