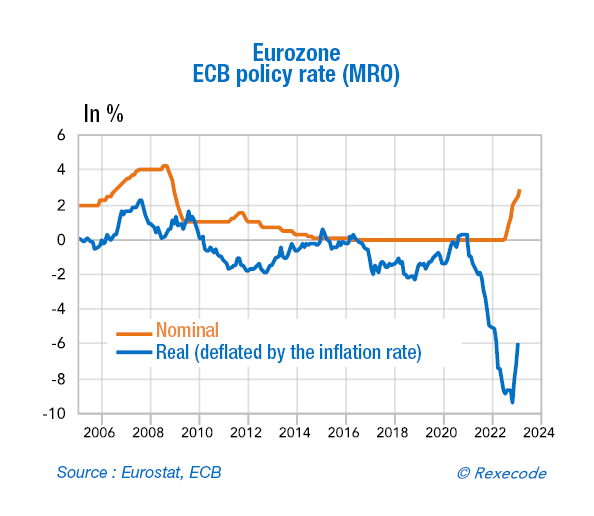

End of negative interest rates: back to normal

The inflation we are currently experiencing will have had at least one good point: the end of zero and negative interest rates. It was indeed irrational to the point that the great economists of the past had never even spoken of it, so incongruous did this possibility seem to them! A negative interest rate means that you are paying to have your money kept, while the logic of the loan is to compensate you for temporarily denying yourself the use of a certain amount of money.

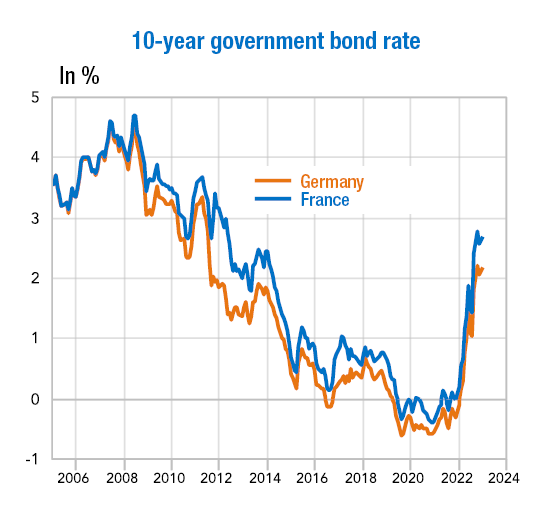

But that’s what we experienced for several years: the interest rate on 10-year French bonds (the benchmark maturity) settled into negative territory from mid-2019 to mid-2021 (spring 2020 being the exception). As for two-year bonds, this situation even persisted from 2014 to early 2022. The same phenomenon has been seen in several other countries in the eurozone, notably Germany. The State then borrowed without paying any interest, and even got paid for doing so!

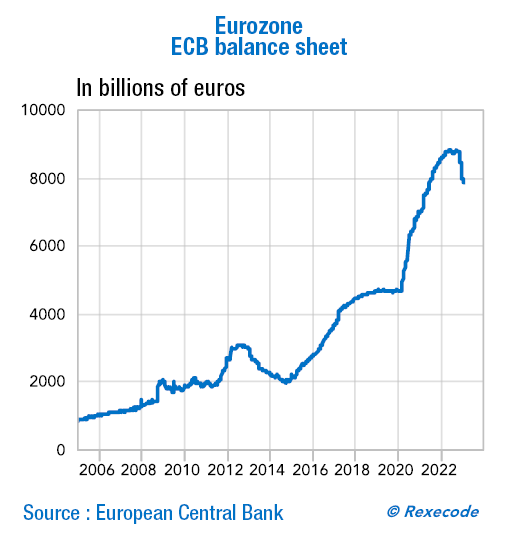

The reason for this phenomenon was the policy of the European Central Bank (ECB) – following its American counterpart, the Fed – which had reduced its key rate to almost zero just after the subprime crisis in order to facilitate the refinancing of the banking system, which was at the time in difficulty, and to support economic activity. The ensuing Greek public debt crisis prompted the ECB to prolong its low rates. At the same time, central banks were buying government bonds in order to lower interest rates on all maturities (2 years, 5 years, 10 years, etc.). How can this be? Simply by creating money. The ECB’s balance sheet has therefore increased from around 1,000 billion euros just before the 2007-2008 crisis to more than 8,000 today. This is called “quantitative easing”.

It worked well, there was more money, more/too much liquidity in the economy, and inflation became a reality. Central banks are now raising their key rates and putting an end to their debt purchases in order to curb inflation. We are back to positive interest rates. However, the situation is not yet completely back to normal because the real interest rate (interest rate – inflation rate), the one that really matters, remains negative. The interest income is still lower than the rise in prices.

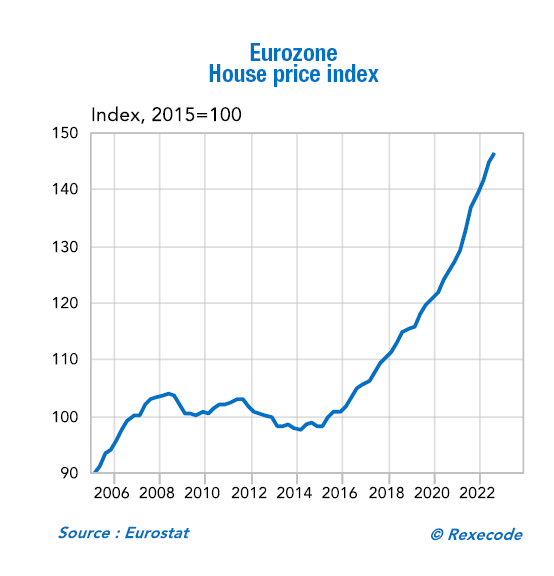

What effects will this reversal have? “Free” money has pushed up the price of tangible assets, which themselves are in limited supply and therefore provide safe havens from monetary expansion (real estate, equities, works of art, collectible cars, commodities, gold, etc.). From now on, some bubbles are in danger of deflating and only quality goods will resist. We will have to become more selective. From now on, precise, meticulous economic analysis will return to the forefront, which is also good news.